Homebuyers looking for homes in the lower and middle price ranges found fewer homes and a lot of competition in the Northern Virginia housing market last month. That trend is expected to continue in 2018.

Homebuyers looking for homes in the lower and middle price ranges found fewer homes and a lot of competition in the Northern Virginia housing market last month. That trend is expected to continue in 2018.

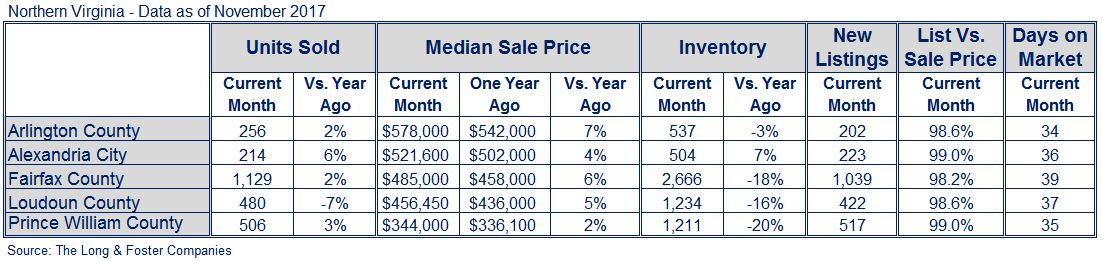

Long & Foster Real Estate’s Market Minute report for Northern Virginia includes the city of Alexandria, and Arlington, Fairfax, Loudoun and Prince William counties.

The ongoing inventory squeeze primarily affects buyers in the lower and mid-level price ranges, with millions among the largest generation in U.S. history – millennials – reaching the stage in life when people form families and buy homes, said Larry “Boomer” Foster, president of Long & Foster Real Estate.

“In the luxury space, there’s plenty of inventory, but entry-level homes – that’s tougher,” Foster said. “There’s no way to build quick enough to meet the demand, and baby boomers are staying in their homes longer than they ever have.”

He recommended buyers work with a real estate agent to prepare for any housing search. A buyer who has received preliminary approval for financing and enlisted the help of an agent who knows the market will have a greater chance at success in getting an offer accepted, he said.

Strong demand and low inventory usually result in price appreciation, and that’s what happened in Northern Virginia in November, continuing the trend of at least the past two years, Foster said. Prices rose countywide, up 2 percent in Prince William County to 7 percent in Arlington County. Meanwhile, inventory fell everywhere except Alexandria. It was down double digits in Prince William, Loudoun and Fairfax counties.

“It’s the same story in Northern Virginia, Washington, D.C., and Montgomery County,” Foster said. “These are almost always very strong, stable markets.”

Foster predicted 2018 would bring more of the same, with strong employment, wage growth and low interest rates expected to remain positive forces in the housing market. Affordability could become more of a concern however, he said. Interest rates are expected to rise modestly, and home prices could continue to go up.

“Owning a home is a great investment and a great way to build wealth,” he said. “If you own a home, you’re in a pretty good place right now.”

Foster said he’s closely watching tax legislation making its way through Congress, to see how homeowners will be affected. Measures to limit the amount of mortgage interest and local property taxes that homeowners could deduct might affect homeowners in the upper end of the market or in high-cost areas.

“It’s hard not to be concerned about that,” Foster said. “But I think people buy homes for reasons other than the tax breaks they might get. They buy homes for the security of having something that’s their own, to have an appreciating asset, to have a place to raise kids and grow their families in.”

The Long & Foster Market Minute is an overview of market statistics based on residential real estate transactions for more than 500 local areas and neighborhoods and over 100 counties in eight states. The easy-to-read, easy-to-share reports include information about each area’s units sold, active inventory, median sale prices, list to sold price ratio, days on market and more.

Information included in this report is based on data supplied by Metropolitan Regional Information System and its member associations of Realtors, which are not responsible for its accuracy. The reports include residential real estate transactions within specific geographic regions, not just Long & Foster sales, and they do not reflect all activity in the marketplace. Information contained in this report is deemed reliable but not guaranteed, should be independently verified, and does not constitute an opinion of MRIS or Long & Foster Real Estate.