Homes on the market in Northern Virginia moved quickly in July as inventory remained low, according to the Long & Foster Market Minute reports. The Northern Virginia market includes the city of Alexandria and Arlington, Fairfax, Loudoun and Prince William counties. The Long & Foster Market Minute reports are based on data provided by Metropolitan Regional Information System and its member associations of Realtors and include residential real estate transactions within specific geographic regions, not just Long & Foster sales.

Homes on the market in Northern Virginia moved quickly in July as inventory remained low, according to the Long & Foster Market Minute reports. The Northern Virginia market includes the city of Alexandria and Arlington, Fairfax, Loudoun and Prince William counties. The Long & Foster Market Minute reports are based on data provided by Metropolitan Regional Information System and its member associations of Realtors and include residential real estate transactions within specific geographic regions, not just Long & Foster sales.

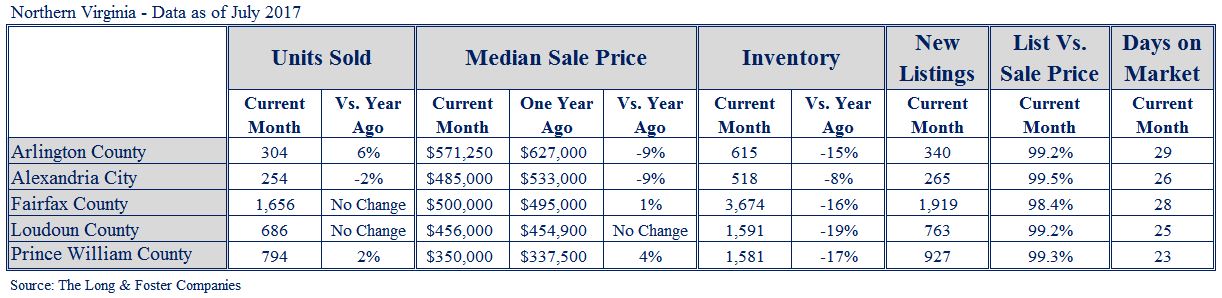

The number of homes sold in the Northern Virginia region varied in July. Arlington and Prince William counties experienced increases of 6 percent and 2 percent respectively. Both Fairfax and Loudoun counties saw no year-over-year change, and in Alexandria City, the number of homes sold fell by 2 percent.

The region’s median sale prices varied in July as well, with Prince William and Fairfax counties seeing increases of 4 percent and 1 percent, respectively. Loudoun County experienced no change from the previous year, and both Arlington County and Alexandria City experienced decreases of 9 percent.

Active inventory declined throughout Northern Virginia. In Loudoun County, active inventory fell by 19 percent, followed by Prince William County with a 17 percent decrease. Fairfax County experienced a 16 percent decline in active inventory, and Arlington County saw a 15 percent decrease. In Alexandria City, active inventory fell by 8 percent.

Homes sold quickly in Northern Virginia last month. Prince William County experienced the lowest days on market (DOM) average at 23 days, while Loudoun County experienced a DOM average of 25 days. In Alexandria City, the DOM average was 26 days, and the DOM average was 28 days in Fairfax County. Arlington County experienced a DOM average of 29 days.

“While many feel optimistic about the U.S. economy as a whole, the issue of low inventory continues to curb the efforts of many who are in the market to buy a home, including homebuyers in the Northern Virginia region,” said Jeffrey S. Detwiler, chief operating officer of The Long & Foster Companies. “The good news is that new home construction has been gradually but steadily increasing, which should help provide some relief, and mortgage rates remain low as we head toward the end of summer.”

The Long & Foster Market Minute is an overview of market statistics based on residential real estate transactions and presented at the county level. The easy-to-read and easy-to-share reports include information about each area’s units sold, active inventory, median sale prices, months of supply, new listings, new contracts, list to sold price ratio, and days on market. Featuring reports for more than 500 local areas and neighborhoods in addition to more than 100 counties in eight states, The Long & Foster Market Minute is offered to buyers and sellers as they aim to make well-informed real estate decisions.

The Long & Foster Market Minute reports are available at www.LongandFoster.com, and you can subscribe to free updates for the reports in which you’re interested. Information included in this report is based on data supplied by MRIS, which is not responsible for its accuracy. The reports do not reflect all activity in the marketplace. Information contained in this report is deemed reliable but not guaranteed, should be independently verified, and does not constitute an opinion of MRIS or Long & Foster Real Estate.