Areas of the Hampton Roads real estate market saw a rising number of homes sold and steady average marketing times in August. Overall, the region’s market is solid and consistent, according to the Long & Foster Market Minute reports. The Hampton Roads region includes Chesapeake, Hampton, Newport News, Norfolk and Virginia Beach cities.

Areas of the Hampton Roads real estate market saw a rising number of homes sold and steady average marketing times in August. Overall, the region’s market is solid and consistent, according to the Long & Foster Market Minute reports. The Hampton Roads region includes Chesapeake, Hampton, Newport News, Norfolk and Virginia Beach cities.

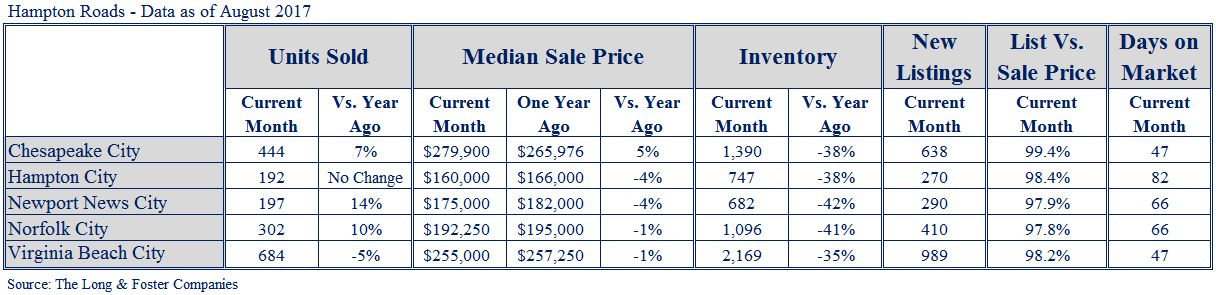

A few areas of the Hampton Roads region saw the number of homes sold rise in August, including the city of Newport News, where home sales increased by 14 percent. Median sale prices dipped slightly in most of the region compared to the same month last year, though Chesapeake City experienced a 5 percent increase.

“The Hampton Roads region, similar to other parts of the Commonwealth, is staying pretty true to what we’re seeing happening throughout the Mid-Atlantic,” said Gary Scott, president of Long & Foster Real Estate. “In recent months, the Hampton Roads market has performed consistently, despite the inventory difficulties being experienced throughout the country.”

Active inventory fell significantly in all parts of the Hampton Roads region in August, with Newport News City seeing a 42 percent drop followed by Norfolk City with a 41 percent drop. Homes in the region sold in six to 12 weeks on average.

“Inventory continues to be a challenge in every market in which we operate, and we believe inventory is an issue that will probably not go away overnight,” Scott said. “There are a lot of people who have financed, refinanced or purchased at very favorable interest rates in recent years, and their motivation is different than it was for many in the past – they’re staying put.”

The inventory shortage is making purchasing a home particularly difficult for millennial buyers, Scott said. That’s not necessarily because millennials and older generations are competing to purchase the same homes, but more due to homeowners and investors choosing not to sell homes that millennials would be interested in purchasing, he said. Although new construction has increased, homebuilders are having a hard time meeting the demands of the market, he said.

“Right now, more people are moving toward smaller more effective, more efficient housing than the big boxes,” Scott said. “There are many millennials looking for maintenance-free, convenient living – like condos and townhouses – that is close to retail, entertainment and work opportunities.”

The best thing that homebuyers can do, Scott said, is to have their financing lined up, have an agent who is an expert negotiator at the ready and remember that real estate is hyperlocal. Within a single large subdivision, it’s possible to see homes in one part of the neighborhood sell quickly while homes in another part sell at a slower pace, he said. Long & Foster’s Market Minute reports allow consumers to view market data for individual communities and neighborhoods. Combining the information from regional and local reports, along with the neighborhood insight and expertise of a Long & Foster agent, can provide a much more rounded and accurate picture of the market, Scott said.

The Long & Foster Market Minute is an overview of market statistics based on residential real estate transactions for more than 500 local areas and neighborhoods and over 100 counties in eight states. The easy-to-read, easy-to-share reports include information about each area’s units sold, active inventory, median sale prices, list to sold price ratio, days on market and more.

Information included in this report is based on data supplied by Real Estate Information Network multiple listing service and its member associations of Realtors, which are not responsible for its accuracy. The reports include residential real estate transactions within specific geographic regions, not just Long & Foster sales, and they do not reflect all activity in the marketplace. Information contained in this report is deemed reliable but not guaranteed, should be independently verified, and does not constitute an opinion of REIN or Long & Foster Real Estate.